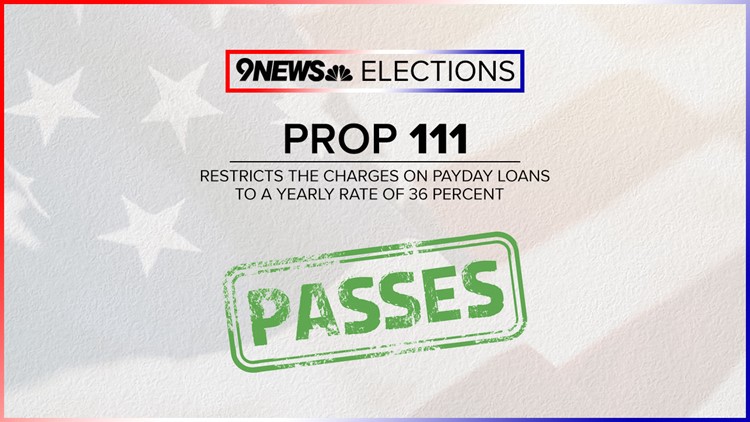

KUSA — Proposition 111, which would lower interest rates to 36 percent from 45 percent (Colo. Rev. Stat. 5-3.1-105) and eliminate all fees associated on payday loans, is projected to pass.

Currently, payday loans—small, short-term loans also called cash advances that are linked to the size of a borrower’s paycheck—have interest rates and fees of 20 percent on the first $300, a charge of 7.5 percent on any amount above $300, a monthly maintenance fee up to $30 a month and an additional annual interest rate of 45 percent. Prop 111, which is slated to take effect Feb. 1, 2019, would put in place a flat interest rate of 36 percent on any amount loaned, according to the Colorado 2018 Blue Book.

A poll conducted three weeks before election day showed Prop 111 with 84 percent support among registered voters with a 3.5 margin of error and a sample size of 800 voters. The University of Colorado's American Politics Research Lab conducted the poll and on YouGov.

A committee, Coloradans to Stop Predatory Payday Loans, spent over $2 million to persuade voters to pass this proposition.

According to the Colorado Blue Book, opposition to the ballot question centered around the fear that these new limitations on APR would effectively kill payday loans in Colorado. Opposition also said more regulations were unnecessary.